Thinking Fast and Slow

Investors tend to act irrational. So what does this mean for your assessment of an investment opportunity and the perception of risk?

Note: this is part of my current PhD research (Vrije Universiteit Amsterdam) on investor decision-making. If you can spare 10 minutes of your time to fill in the anonymous survey it would very helpful. Even if you are not a VC your participation would be highly valued as this provides insights on other investor types acting in a VC context. Every completed qualified response gets a 6 month Premium Upgrade on the Qapital Substack.

Link to survey: https://vuamsterdam.eu.qualtrics.com/jfe/form/SV_bOdxnDOFoKXYmiO

Every investor believes they assess risk analytically. You read the deck, you build the model, you weigh the evidence, you arrive at a number. Disciplined. Objective.

Now look at what you are actually working with in an early-stage deal. No track record. No stable revenue. A market that may not exist yet. The traditional tools of financial analysis need history, and there is none. And yet investors still produce a confident view on how risky the thing is, often within minutes.

So where does that number come from?

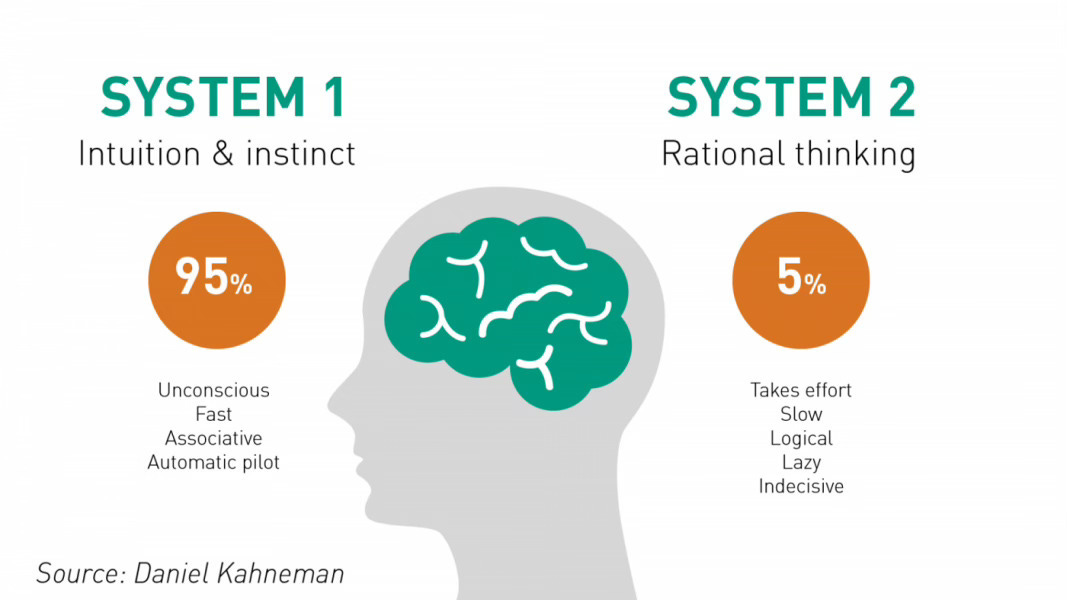

The model is the alibi, not the engine

The uncomfortable answer is that most of an early-stage risk call is a feeling, produced fast, before the analysis begins. We form an intuitive read almost instantly, and then our slower, rational mind goes to work, not to test that read, but to justify it. The spreadsheet arrives after the verdict. It is the alibi, not the engine.

This is not a knock on intuition. Under deep uncertainty, pattern recognition is often all you have, and experienced investors have a lot of it. The problem is what we do with it. We mistake the feeling for analysis, and then we trust it more than we should.

We do not understand our own decisions

Here is the part that should give any serious investor pause. Research on venture capitalists has shown, repeatedly, that they are poor at explaining their own decision process. Ask them which factors drove a call, and their stated reasons often do not match what actually moved them. Worse, experience does not reliably fix this. More experience tends to produce more confidence, not necessarily more accuracy. The most seasoned investors are often the most certain, and certainty is exactly the state in which you stop checking.

So the risk number at the bottom of your memo is not the output of a clean process you can inspect. It is the output of a process you largely cannot see.

Why this owns your valuation

This is not a soft, psychological aside. It is the whole ballgame for price.

Perceived risk is the discount you apply. The riskier it feels, the more return you demand, and the less you will pay. If the perception is an intuition you cannot introspect, then a large part of your valuation discipline is sitting downstream of a feeling you have never actually examined. You are not pricing the venture. You are pricing your reaction to it, and calling it the venture.

What to do with it

You cannot turn the intuition off. You can stop letting it pass unchecked.

Separate what you know from what you feel. Write down the hard facts you actually have, then, separately, the story you have layered on top. The gap between them is where the risk number is really being set.

Distrust your fastest, firmest verdicts. The deals you are instantly sure about, in either direction, are where your rational mind is rubber-stamping rather than working.

Go hunting for the fact that kills the deal. Your instinct will supply the supporting evidence for free. It will never volunteer the disconfirming kind.

Watch your own experience. The more pattern recognition you carry, the more quietly it can override the evidence in front of you. Confidence is not calibration.

The investors who compound are not the ones with no instincts. They are the ones who know their risk number is a feeling first, and who do the work to find out whether the feeling is right.

One ask

This is what I research for my PhD at Vrije Universiteit Amsterdam: how investors actually assess the risk of early-stage ventures, and what really drives the call.

I am close to my sample and need a small number more respondents. If you invest in early-stage ventures, at Seed, Series A, or Series B, I would value about 10 minutes of your judgment in a short, fully anonymous decision experiment. Even if you are not a VC your participation would be highly valued as this provides insights on other investor types acting in a VC context. You will see how your own risk calls behave, and I will share the findings with everyone who completes the survey.

Link to survey: https://vuamsterdam.eu.qualtrics.com/jfe/form/SV_bOdxnDOFoKXYmiO

And if this is not you, but you know an investor who fits, forwarding this is the most useful thing you can do. Thank you.